Supply Signal

The Walls Went Up: How the Chip Industry Picked Sides in One Week

By Semibuffer Intelligence | March 29, 2026 | 12 min read

Last week, Supply Signal Radar reported the five-year sentence: SK Hynix's chairman told the world the memory shortage lasts until 2030. This week, the industry responded — and the responses were structural, not tactical.

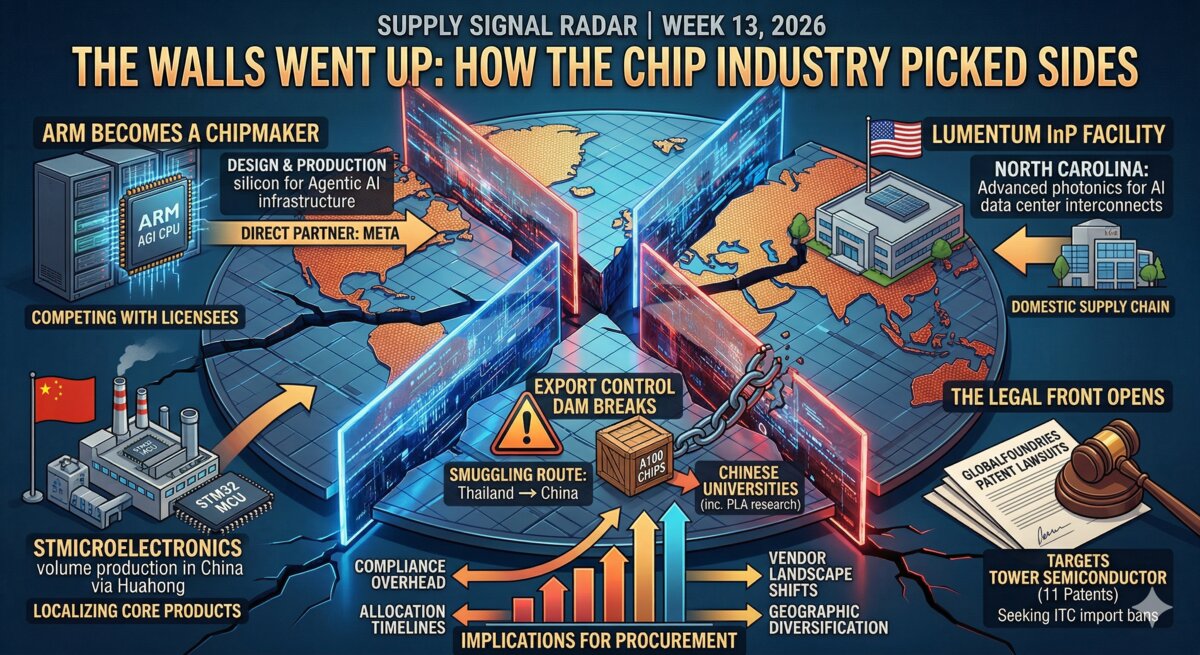

Arm designed its first chip. STMicroelectronics started manufacturing microcontrollers in China. Lumentum broke ground on a new U.S. facility. ASML delivered the world's most advanced lithography system. GlobalFoundries filed patent lawsuits to block imports. And the export control regime cracked further open as Chinese universities were caught acquiring sanctioned Nvidia hardware through the same channels the U.S. just indicted people for using.

In a single week, the semiconductor industry drew new lines — geographic, corporate, and legal. Everyone picked a side. The map changed.

Arm Becomes a Chipmaker

The biggest structural shift this week didn't come from a factory or a courtroom. It came from a company that has spent its entire 35-year existence not making chips.

Arm announced its first-ever production silicon product: the Arm AGI CPU, a data center processor designed for agentic AI infrastructure. The company claims more than 2x performance per rack compared with x86 platforms. Meta is the lead partner, with other ODMs committed to production.

The timing matters. In a market where memory is constrained through 2030 and AI infrastructure demand is consuming every available wafer, Arm decided that licensing IP isn't enough. It needs to control the silicon itself. Meta — one of the world's largest AI infrastructure buyers — chose to partner directly rather than go through intermediaries.

Arm entering production silicon puts the company in direct competition with its own licensees. Qualcomm, MediaTek, and every other Arm licensee building server chips just got a new competitor that also controls their instruction set. For procurement teams specifying server hardware for 2027 and beyond, the vendor landscape you're quoting from is about to change.

Manufacturing Geography Shifts

While Arm was restructuring the corporate architecture of chips, two other moves were quietly reshaping where chips get made.

STMicroelectronics began volume production of STM32 microcontrollers in China through a partnership with Huahong. The STM32 is one of the most widely used microcontroller families in industrial and embedded applications — it's in everything from motor controllers to medical devices to factory automation systems. Moving production to China puts STM closer to its largest customer base, but also inside a trade environment that is becoming more compartmentalized by the month. For buyers, this means China-manufactured STM32s may carry different lead times, compliance documentation, and sourcing implications than European-manufactured ones. Worth tracking which fab your allocations come from.

Lumentum announced a new manufacturing facility in North Carolina for Indium Phosphide (InP) laser devices targeting AI data center optical interconnects. This is the opposite geographic vector — pulling advanced photonics manufacturing back into the U.S. for the AI buildout. InP devices are critical for the high-bandwidth optical links that connect GPU clusters in AI data centers. Domestic production means shorter lead times for U.S.-based hyperscalers and reduced exposure to cross-border supply risk.

A third signal reinforced the geographic shift: a new $2 billion vertically-integrated AI cloud venture in Japan, founded by former Tenstorrent executives. Japan, which has been aggressively rebuilding its semiconductor manufacturing base, is now attracting AI infrastructure capital at scale.

Three moves. Three continents. China, the U.S., and Japan — each pulling semiconductor manufacturing capacity toward their own markets. The shared supply chain that defined the last two decades of globalization is fragmenting into regional blocks.

The Export Control Dam Breaks

The Super Micro story that we tracked last week — three employees indicted for a $2.5 billion smuggling operation — escalated significantly.

Shareholders filed a securities fraud lawsuit against Super Micro, alleging the company "concealed dependence on illicit sales to China." The complaint claims that illegal activities constituted "a huge portion" of the company's revenue. Separately, three more individuals were charged with conspiring to smuggle servers containing controlled chips to China by routing them through Thailand on paper while shipping to China as the final destination.

And then the most damning signal: public documents revealed that four Chinese universities — including two conducting military research for the PLA — acquired servers containing sanctioned Nvidia A100 chips, with purchases completed in 2025 and 2026 despite U.S. export controls.

The enforcement apparatus is tightening and the evasion networks are being exposed simultaneously. For procurement teams, this means compliance requirements will intensify, end-use documentation will face more scrutiny, and allocation timelines for any AI-adjacent hardware will lengthen. The era of treating export controls as a paperwork exercise is over.

The Equipment Race Continues

Two signals this week pointed to the next generation of manufacturing capability being deployed — and the next generation after that being funded.

ASML delivered the EXE:5200 High-NA EUV lithography system to imec's 300mm cleanroom in Leuven, Belgium. This is the most advanced lithography tool in the world — the machine that will define what's physically possible to manufacture at the leading edge for the next several years. Imec, as the industry's premier R&D consortium, will use it to develop the processes that TSMC, Samsung, and Intel will eventually run in production.

High-NA EUV is the gating technology for sub-2nm chip manufacturing. The fact that the first production-grade system is now installed means the process development clock has started. Production adoption is likely 2028–2029, which aligns with the SK Hynix chairman's 2030 shortage timeline — even the most advanced new capacity takes years to reach meaningful volume.

Meanwhile, Lace Lithography raised $40 million in Series A funding for helium atom beam lithography — a technique that uses a 0.1nm beam (135 times narrower than ASML's EUV light) to pattern wafers at atomic resolution. Microsoft is a backer. This is R&D-stage technology with no near-term production impact, but it signals that serious capital is flowing into alternatives to the ASML-dominated lithography ecosystem.

The Legal Front Opens

GlobalFoundries filed patent infringement lawsuits against Tower Semiconductor, asserting 11 U.S. patents across three separate filings — two in the Western District of Texas and one with the U.S. International Trade Commission (ITC). The lawsuits seek to halt the importation and sale of semiconductors that GF alleges infringe its patented technologies. GF has used this playbook before, most notably in its 2019 campaign against TSMC.

This adds a new dimension to supply chain risk: legal risk. In a market where every available chip matters, patent injunctions that block imports — even temporarily — can cascade through allocation queues.

What This Week Means

Week 13 was the week the semiconductor industry stopped debating the crisis and started building walls.

Arm walled off its own silicon. STM walled off its China production. Lumentum walled off its U.S. photonics capacity. Export control enforcement walled off AI hardware from sanctioned buyers — while simultaneously exposing how porous those walls remain. GlobalFoundries used patent law to build legal walls around its IP.

Every one of these moves is a response to the same underlying condition: a market where supply is structurally constrained through 2030, demand is accelerating, and the rules of global trade are being rewritten in real time.

For procurement teams, the practical implication is this: the supply chain you planned around six months ago may not exist in the same form six months from now. Geographic diversification, vendor qualification, and compliance documentation are no longer nice-to-have operational improvements. They are existential requirements.

The walls went up this week. Where you stand relative to them determines what you can buy, when, and from whom.

This analysis was produced by Semibuffer's intelligence pipeline — daily AI-powered monitoring of SEC filings, trade publications, and supply chain signals, synthesized by our team.