Supply Signal

$200 Billion and Counting: The Semiconductor Industry's Most Expensive Year, Ever

By Semibuffer Intelligence | April 5, 2026 | 14 min read

Last week, Supply Signal Radar reported the walls going up — Arm entering production silicon, STMicro manufacturing in China, ASML delivering High-NA EUV to U.S. soil. This week, the bill arrived.

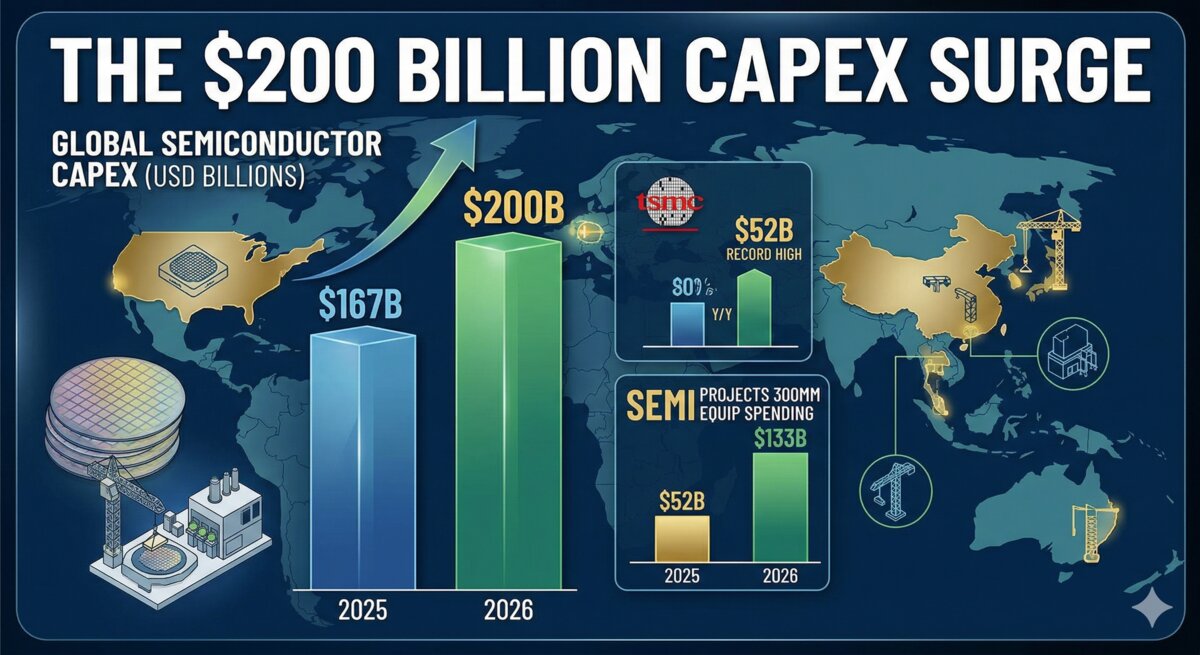

Global semiconductor capital expenditure is projected to surge 20% to $200 billion in 2026. TSMC alone is targeting $52 billion — and reportedly planning to expand its Arizona presence to 12 fabs and four packaging facilities. SEMI projects 300mm equipment spending will hit $133 billion this year and $151 billion next year. Intel just paid $14.2 billion to buy back Apollo's stake in its Irish fab, at a $3 billion premium, while its balance sheet is already under pressure.

The industry is spending at a pace it has never attempted before. And in the same week, a NOR Flash shortage emerged as a collateral casualty of the memory crisis, counterfeit AI chips entered the market because real ones can't be found, and the PC market is projected to contract 13% because the components to build them cost too much.

Everyone's building. Nobody has enough. The fakes are filling the gap.

The $200 Billion Year

Two data points this week framed the scale of what's underway.

Global semiconductor CapEx is projected to hit $200 billion in 2026, up 20% year-over-year. TSMC is the largest single contributor at $52 billion — a record for any foundry in any year. The spending is concentrated in leading-edge logic and advanced packaging for AI infrastructure, which means the capacity being built serves a specific customer set: hyperscalers, AI infrastructure builders, and the supply chains that feed them.

Separately, SEMI projects 300mm fab equipment spending will grow 18% to $133 billion in 2026 and another 14% to $151 billion in 2027. Two consecutive years of double-digit equipment spending growth is a supercycle by any definition. The last time equipment spending grew at this rate for this duration was 2020–2021, and that cycle ended with the inventory correction of 2022–2023.

The difference this time: the spending is being driven by structural demand (AI infrastructure) rather than pandemic pull-forward. Whether that makes the buildout more durable or simply means the eventual correction will be larger is a question the industry hasn't answered yet.

Then came the Arizona signal. Reports emerged that TSMC is planning to expand its U.S. footprint to 12 fabs and four advanced packaging facilities in Arizona — potentially the largest foreign foundry buildout in U.S. history. Confidence on this signal is low (early-stage reports, likely tied to broader Taiwan-U.S. investment negotiations), but the direction is unmistakable: TSMC is building a second manufacturing base, and it's in the American Southwest.

For procurement teams, the equipment supercycle has a direct implication: if your supply chain depends on fab equipment, construction materials, specialty gases, or cleanroom infrastructure, those resources are being absorbed by the buildout. Lead times for fab-adjacent services and materials will extend. Lock in contracts now for 2027 deliveries.

Intel's $14.2 Billion Gamble

Intel repurchased Apollo's 49% stake in Irish Fab 34 for $14.2 billion — a $3 billion premium over the original deal value. The transaction gives Intel full ownership and control of the facility, removing joint-venture governance complexity.

The strategic logic is straightforward: Intel wants unencumbered control of a leading-edge fab as it tries to build Intel Foundry Services into a credible third-party manufacturing option. Fab 34 in Leixlip, Ireland produces Intel 4 and Intel 3 process technology.

The financial logic is harder to defend. Intel paid a $3 billion premium at a time when the company's balance sheet is already stretched. The buyback increases Intel's debt load precisely when it needs financial flexibility to fund its broader foundry ambitions — including fabs in Ohio, Germany, and the ongoing Arizona expansion. Every dollar spent on the Apollo buyback is a dollar not available for the equipment, talent, and R&D that Intel Foundry needs to compete with TSMC and Samsung.

What this means for procurement: If you source from Intel Foundry Services or are evaluating IFS as a foundry option, the Fab 34 consolidation simplifies the decision-making structure — one owner, one roadmap. But watch Intel's quarterly financials closely. The company's ability to fund simultaneous fab buildouts across three continents while absorbing a $14.2 billion buyback will determine whether IFS capacity ramps on schedule or slips.

The Shortage Spreads Sideways

The memory crisis that's dominated Supply Signal Radar for weeks found two new expression points this week — one expected, one alarming.

NOR Flash is now in a shortage. Memory manufacturers' prioritization of DRAM and NAND production is squeezing NOR Flash wafer capacity and backend test resources. NOR Flash doesn't get the headlines that DRAM and HBM do, but it's critical infrastructure: automotive ECUs use it for boot firmware, industrial controllers depend on it for code storage, and IoT devices require it for reliable non-volatile memory. When DRAM and NAND wafer starts take priority — because margins are higher and AI demand is insatiable — NOR Flash gets the leftover capacity.

This is a textbook second-order shortage. The crisis in one segment starves an adjacent segment that shares manufacturing resources. Procurement teams in automotive and industrial electronics should audit NOR Flash inventory positions now and consider extending safety stock. Lead times are extending and won't recover until the memory allocation pressure eases — which, per SK Hynix's chairman, means 2030.

Counterfeit AI chips have entered the market. Hardware shortages in AI accelerators and GPUs have made counterfeiting economically viable. The signal is low-confidence (no specific bust or seizure cited), but the structural logic is sound: when legitimate supply can't meet demand and prices are elevated, counterfeit markets emerge. It happened with passive components in 2021. It happened with automotive MCUs in 2022. Now it's happening with AI silicon.

For procurement teams sourcing AI accelerators through spot markets or non-authorized channels, this means hardware authentication steps are no longer optional. The shortage is severe enough that fakes are worth making — and that's a direct measure of how tight the market has become.

And the demand side is cracking. Omdia forecasts a 13% contraction in U.S. PC sales in 2026, driven by the same chip shortages and memory price increases that are fueling the rest of this crisis. The Windows 10 end-of-life upgrade cycle gave PCs a brief Q4 2025 lift, but the underlying economics are punishing: memory costs are too high for OEMs to maintain margins at current price points. This is demand destruction — not a demand pause. When components cost too much, products don't get built.

The Geopolitical Map Sharpens

Four signals this week added definition to the geopolitical picture that's been developing all quarter.

Supermicro's Wally Liaw pleaded not guilty to AI hardware smuggling charges. This is the continuation of the case Supply Signal Radar tracked in W12 and W13 — the $2.5 billion smuggling operation, the securities fraud lawsuit, the executive-level prosecution. The not-guilty plea means this case will play out publicly over months, keeping compliance scrutiny elevated across the entire AI server supply chain.

Chinese semiconductor leaders publicly acknowledged a five-to-ten year lag in AI data center chips. This is significant because it's a candid admission from inside China's semiconductor ecosystem. AI-driven demand is creating bottlenecks across equipment, passive components, and workforce capacity domestically. Near-term, it reduces competitive pressure from Chinese fabs on leading-edge AI chip supply. But it also means sustained Chinese demand for equipment and passives on the open market, competing with non-Chinese buyers for already-constrained components.

The WTO digital trade moratorium lapsed. The Ministerial Conference in Yaoundé failed to extend the longstanding prohibition on duties for digital trade. This creates potential tariff exposure for semiconductor design IP, EDA software licenses, and cloud-based chip design services that flow across borders. Fabless companies and IP licensors with global royalty flows should assess exposure now.

Japan's power semiconductor sector is consolidating. Rohm has joined Toshiba and Mitsubishi Electric in a power chip partnership, potentially creating a dominant Japanese supplier of IGBTs, SiC devices, and power MOSFETs. For automotive and industrial procurement teams heavily sourced from Japanese power device makers, this is a concentration risk signal worth tracking.

Two additional signals round out the week: Nvidia invested $2 billion in Marvell and partnered on NVLink Fusion, embedding itself into the custom ASIC supply chain of the very hyperscalers trying to reduce Nvidia GPU dependence. And Tower Semiconductor announced 300mm capacity expansion in Japan, adding specialty analog capacity in a geopolitically stable location. Rambus unveiled an HBM4E controller at 16 GT/s and 4 TB/s per stack, advancing ecosystem readiness for next-generation AI memory.

What This Week Means

Week 14 is the week the semiconductor industry's ambitions collided with its constraints.

$200 billion in CapEx. Twelve TSMC fabs in Arizona. Intel spending $14.2 billion it arguably can't afford. These are the ambitions. NOR Flash going short. Counterfeit AI chips appearing. PC sales collapsing 13%. The WTO letting digital trade protections lapse. These are the constraints.

The two lists are related. The industry is spending at historic levels because the demand is real — AI infrastructure, geopolitical reshoring, and a decade-long memory shortage create powerful incentives to build. But the spending itself is absorbing resources (equipment, materials, talent, capital) that the rest of the industry needs to function. The supercycle creates the shortages it's trying to solve.

For procurement teams, the actionable frame is this: audit your exposure to two things. First, fab-adjacent supply chains (equipment, gases, construction, chemicals) that are being consumed by the buildout. Second, second-order shortages like NOR Flash that emerge when memory manufacturers redirect capacity toward higher-margin segments. Both will define availability for the rest of 2026.

The industry just crossed $200 billion in annual spending. The question isn't whether the buildout will continue — it will. The question is whether your supply chain is positioned to benefit from it, or to be starved by it.

This analysis was produced by Semibuffer's intelligence pipeline — daily AI-powered monitoring of SEC filings, trade publications, and supply chain signals, synthesized by our team.