Supply Signal

The Spike Became the Baseline. The Cost Reached the Whole Board.

By Semibuffer Intelligence | June 28, 2026 | 7 min read

The waiting reflex is gone.

For two weeks, memory buyers moved from locking direct supply to crowding into the channel. This week showed what comes after that. Cost pressure stopped behaving like a memory-only problem and started moving through the whole bill of materials.

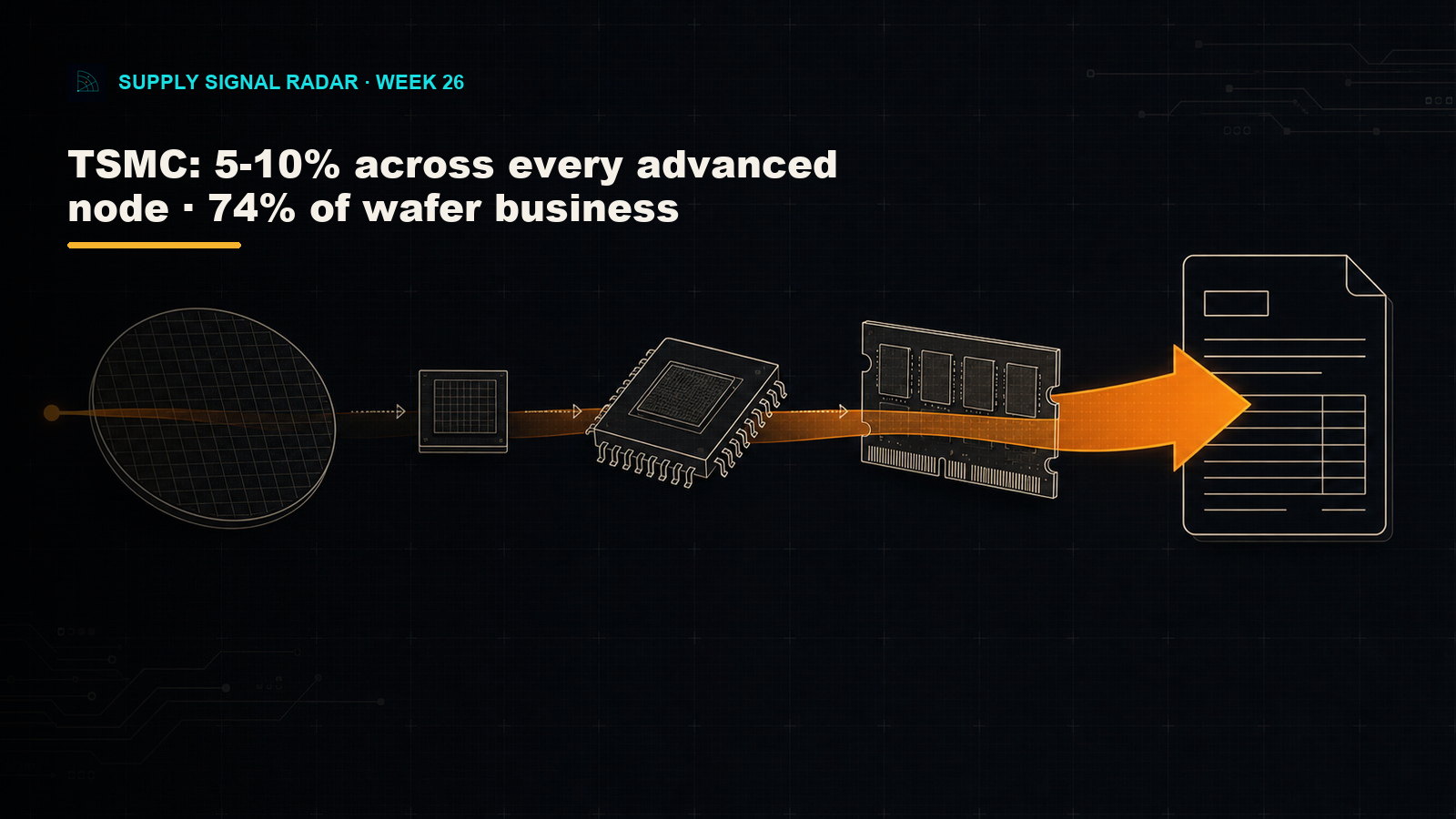

The clearest marker was TSMC. The company was reported to be preparing 5-10% price increases across its advanced-node stack, including 3nm, 7nm, and some legacy processes. The reported scope covers nodes tied to roughly 74% of TSMC's wafer business. That puts Nvidia, AMD, Apple, Qualcomm, and other large customers in the same cost conversation, but the procurement consequence is wider than those names.

If foundry cost resets, finished-board cost resets. Application processors, AI accelerators, networking silicon, premium connectivity, high-end MCUs, and custom ASICs all carry some version of that exposure. Memory is still tight. Now the silicon around it is getting repriced too.

For procurement, the useful conclusion is simple: do not treat this as a temporary memory surcharge. The board cost base moved.

The Foundry Cost Base Moved

That increase matters because of where it lands. A 5-10% wafer-price move is not the same as a spot-market memory quote. It travels through die cost, package cost, module cost, margin protection, and customer pass-through.

That is why the percentage can look modest at the wafer level and still matter at the BOM level. Most procurement files do not buy wafers. They buy finished components, modules, boards, and systems. By the time a foundry price move reaches those quotes, it has passed through every supplier that is trying to protect margin while also competing for scarce capacity.

The timing also matters. The last two weeks already showed buyers securing memory early and using the channel when direct allocation was not enough. A foundry reset does not replace that pressure. It broadens it.

This is the part that should change the RFQ file. A buyer who isolates memory inflation in one line item will understate the actual exposure. The same board may now carry DRAM pressure, NAND pressure, advanced-node pressure, packaging pressure, and supplier margin pressure at the same time.

The quote may still arrive as a component-level delta. The decision has to be board-level.

The Old Memory Is Not the Cheap Memory

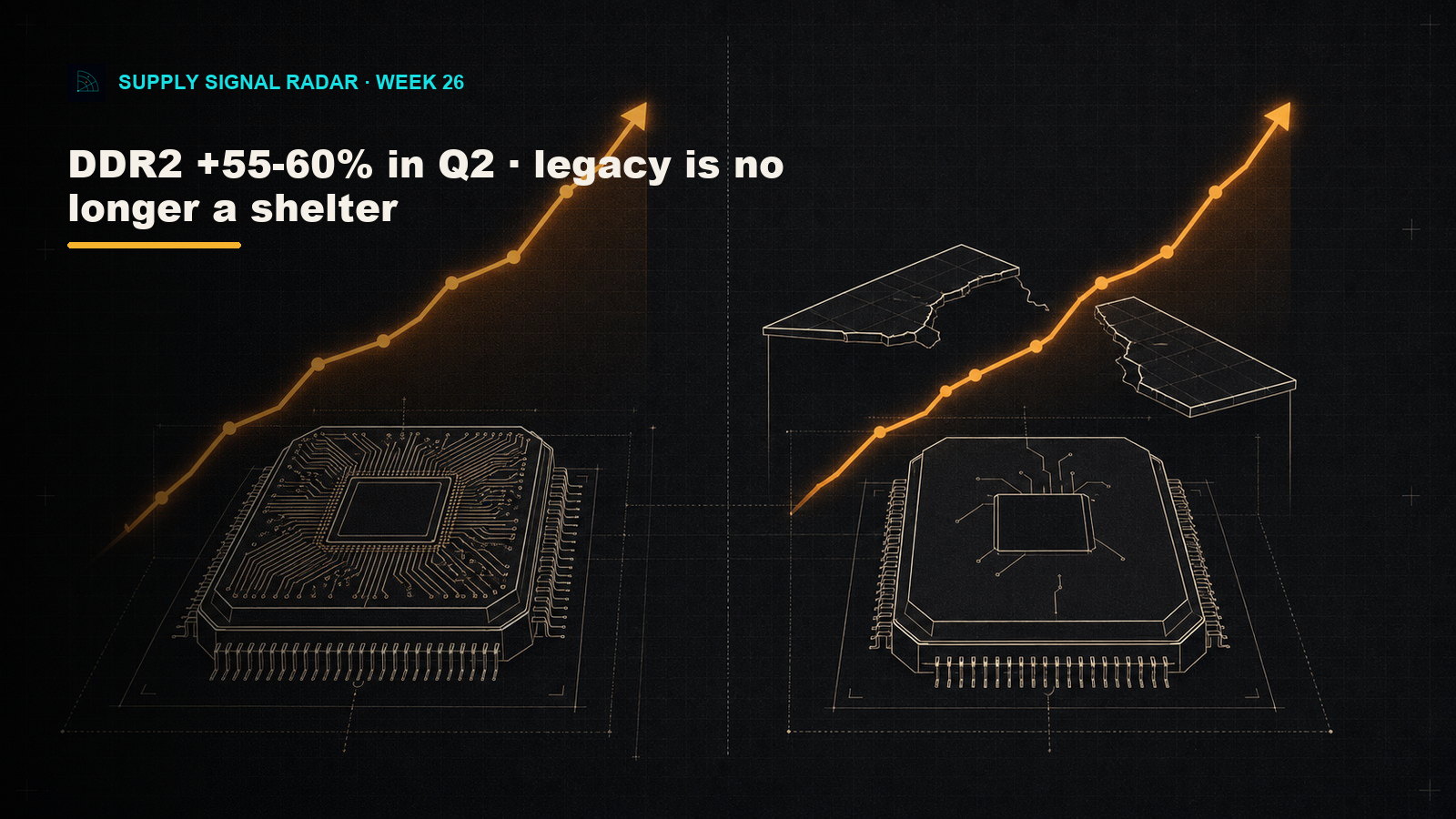

The memory pressure did not stay in HBM, DDR5, or AI server builds. DDR2 contract prices reportedly jumped 55-60% in Q2, with another 35-40% increase projected for Q3.

That is the sharper procurement warning. DDR2 is not the part of the market buyers usually associate with frontier AI demand. It sits in older, cost-sensitive, long-life products where redesigns are slow and approved alternates are limited. When that lane reprices this hard, legacy is no longer a shelter.

Lenovo gave the moment a blunt name: "RAMageddon." The wording is colorful. The behavior underneath is more important. Buyers are no longer asking whether memory pricing will normalize quickly. They are starting to plan around a higher floor.

Commodore's Callback flip phone showed what that looks like downstream. The product moved its base price from $499 to $399 by defaulting to recycled memory chips and moving accessories out of the default bundle. That is an end product rewriting its bill of materials because memory cost reached the shelf — the squeeze surfacing where the retail price is visible.

That matters for industrial and medical buyers too. A cost reset in old memory can show up first in consumer electronics because the retail price is visible, but the same parts sit inside long-life controllers, displays, gateways, point-of-sale equipment, test gear, and replacement programs.

The old assumption was that mature memory was cheap because it was mature. This week made that assumption harder to defend.

The Majors Are Funding the Squeeze

The supply side did not answer the squeeze by waiting it out.

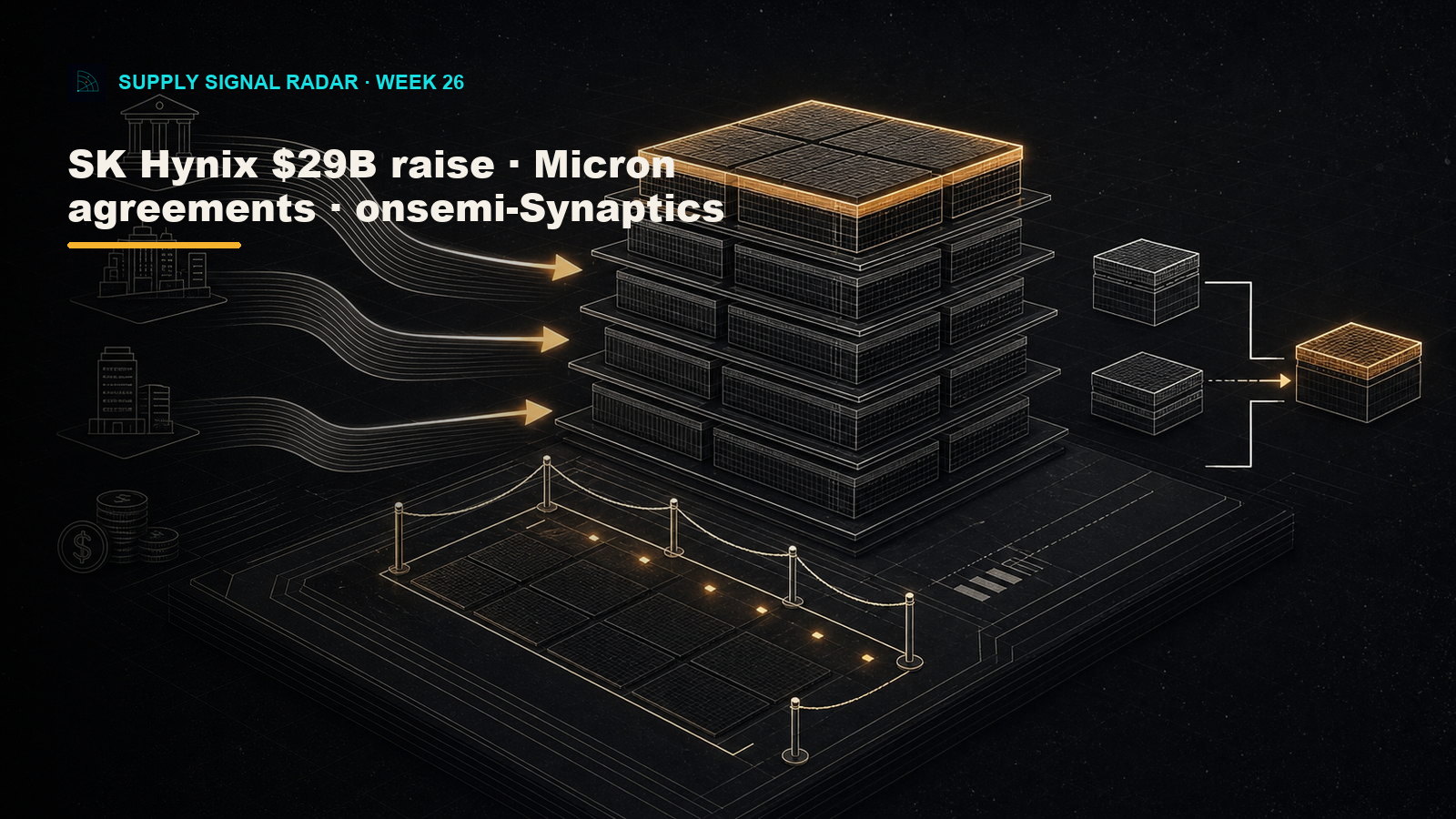

SK Hynix filed to raise up to $29 billion through a Nasdaq ADR listing to support AI-memory fabs and EUV investment. Micron reported record quarterly results and pointed to strategic customer agreements that are reshaping how large buyers secure memory. onsemi agreed to acquire Synaptics, adding connected compute and control capability to a portfolio already built around power and sensing.

These are different stories on the surface. Together, they show the same posture. Suppliers are committing capital, locking customer structures, and buying capability around the parts of the market where demand is strongest.

That is useful for buyers, but only if it is read correctly. More investment does not mean near-term allocation opens up evenly. It often means the best customers get earlier structure, firmer volume, and clearer commercial terms while everyone else waits for the second pass.

The onsemi-Synaptics deal belongs here because the pressure has spread past memory. Physical AI, edge devices, industrial automation, automotive platforms, and connected products all need more sensing, control, power, memory, and compute in the same system. Suppliers are positioning for that system-level demand.

Qualcomm's data-center push points in the same direction. Export-compliant China variants and new AI infrastructure products do not remove demand from the market. They create more qualified demand surfaces that still pull memory, substrates, power, networking, and advanced-node capacity.

Every one of those moves is capital committing to a higher cost base.

What to Watch For

These are the conditions we are tracking to tell whether the cost reset broadens or stalls.

- TSMC confirmation and pass-through timing. The foundry increase matters most when it starts appearing in customer quotes, distributor updates, and supplier cost-change notices.

- Legacy DRAM in Q3. Our standing view has been that contract DRAM pricing rises more than 10% quarter over quarter in this period. DDR2's Q2 move is the loudest confirmation so far. The next read is whether the Q3 step stays concentrated in legacy memory or spreads across specialty and mainstream parts.

- Memory substitution in finished products. More OEMs changing memory grades, reducing bundled accessories, delaying high-memory configurations, or moving to recycled and alternate sourcing lanes signals the reset reaching the shelf.

- Strategic customer agreements. If more memory suppliers describe direct customer structures, pre-committed volume, or preferred allocation, smaller buyers should assume the open market is getting thinner.

- AI infrastructure SKUs outside the GPU. Qualcomm, Micron, SK Hynix, onsemi, and TSMC point to the same practical issue: AI demand is pulling the board, not just the accelerator.

- The demand ceiling. The honest crack in the setup is affordability. If PCs, phones, and edge devices keep losing low-cost configurations, demand can weaken at the bottom even while allocation stays tight at the top.

What To Do This Week

- Re-run board-level should-cost with both memory and foundry assumptions. Do not leave the reset inside the DRAM line.

- Separate memory exposure by generation and product life. DDR2, DDR3, DDR4, LPDDR, NAND, and HBM now need different escalation assumptions.

- Ask suppliers which part of the quote is temporary and which part is a new baseline. Put the answer in the commercial file before the next customer price discussion.

- Re-quote alternates on mature-node and legacy-memory parts before Q3 pricing is locked. The cheap alternate may not stay cheap.

- Review pass-through clauses with sales and finance. A board-level cost reset needs a board-level customer conversation.

- Pre-approve substitution rules for low-margin products. If recycled memory, alternate memory grades, or bundle changes are acceptable, decide that before shortage pricing forces the decision.

First the shortage forced buyers to lock supply. Then it pushed them into the channel. This week it settled into the cost base.

A buyer still treating memory inflation as a temporary line-item problem is now underpricing the finished product. The next quote may not be a spike. It may be the new floor.

Supply Signal Radar is the free weekly brief at semibuffer.com/radar. Signal Chat is coming soon — direct conversational access to the intelligence underneath these analyses. Subscribers go first.

Sources: Tom's Hardware on TSMC reported wafer-price increases, DDR2 pricing, SK Hynix financing plans, Lenovo's "RAMageddon" comments, and Commodore Callback memory changes; Micron's Q3 FY26 results; onsemi's Synaptics acquisition release; EE Times on Qualcomm data-center solutions; and Tom's Hardware on Qualcomm China-specific data-center chips. Published weekly by Semibuffer Intelligence.

Related Episodes

- Week 26: The Spike Became the Baseline — The Cost Reached the Whole Board: Week 26: TSMC is reported to be hiking every advanced node and DDR2 jumped 55-60%, so the memory spike stopped being a line item and reset the whole bill of materials. The majors are financing a higher cost base — SK Hynix's $29B raise, Micron agreements, onsemi-Synaptics.